Written Commentary

Eurozone inflation readings from Germany and France along with Services PMIs will be the statistical focal point for the day, as yesterday’s December FOMC minutes are digested, with little else in the way of central bank events scheduled. Markets may perhaps take rather more than was intended from this section of the minutes: “Several participants remarked that the Committee’s balance sheet plans indicated that it would slow and then stop the decline in the size of the balance sheet when reserve balances are somewhat above the level judged consistent with ample reserves. These participants suggested that it would be appropriate for the Committee to begin to discuss the technical factors that would guide a decision to slow the pace of runoff well before such a decision was reached in order to provide appropriate advance notice to the public.” The key word is ‘several’ indicating a very small minority of FOMC participants, and given the prior experience of ending QT, and the eventual significant disruption to money markets, above all repo markets, it should thus come as little surprise that they are likely concerned about avoiding any form of repeat.

The challenge for the Fed, which has argued that QT is a largely mechanical process, is how such a discussion is communicated to markets without supercharging markets’ ‘animal spirits’. It is made all the more complicated by the fact that there is a very complex interplay in overall market liquidity between the Fed’s balance sheet, bank reserves and the Treasury’s balance at the Fed, as can be seen in the attached chart. Be that as it may, markets will likely view this as a further ‘dovish’ shift, though some may argue that opening such a discussion at such an early stage may be indicative of some Fed concern about financial stability.

Today’s German and French HICP are both expected to rise 0.3% m/m, though the -0.1% m/m drop in NRW state CPI imparts downside risks for national CPI, but adverse base effects in household energy costs and road fuel prices is expected to drive German y/y sharply higher to 3.9% from a flattering 2.3% in December, and edge French y/y up to 4.1% from 3.9%. The former is in turn expected to see tomorrow’s headline Eurozone CPI jump to 3.0% y/y from 2.0%, though core is forecast to dip further to 3.4% y/y from 3.6%, which in ECB policy outlook terms would be more significant than the persistent base effect paced noise in headline readings. A third consecutive m/m and larger than expected rise in China’s Services to 52.9 from 51.4 may prove to be the most significant it terms of the array of Services PMI, though it remains well below the range of outturns in H1 2023, and sluggish on any historical comparisons. The Eurozone reading is seen unrevised at 48.1, as are the more buoyant readings in the UK (52.9) and USA (51.3).

The most important elections are likely to be those in USA, India, Indonesia, Iran, Mexico, Pakistan, South Africa, U.K. and the EU. The US election will be the most divisive since at least 1968, with the current presumption being that it will be between Biden and Trump. However given that both are ageing, and Trump’s legal challenges, the chances that one or both do not make it through to November 5 election day is quite high. The UK election timing remains uncertain, and while the opposition Labour party holds a large opinion poll lead, a pre-Christmas poll showed the public has an overall unfavourable opinion of both PM Sunak (51%) and Labour leader Starmer (42%). Indian PM Modi would appear to be on course for a decisive 3rd term victory, though the seemingly fickle voting public has often sprung surprises in the past. The EU Parliament elections will above all be about whether the centre can hold onto overall control, given sharp swings to the populist/extreme right or left in many countries, failure would raise questions not only over much needed EU reforms, but also about its longer-term existence.

Increasingly ambivalent Western (EU/US) support for Ukraine begs the question about when western leaders may start to increase pressure on Ukraine to agree a peace treaty with Russia and cede control of eastern and southern parts to Russia, perhaps all the more so given the electoral uncertainties noted above. The fact that this would further undermine the already heavily tarnished authority of the US, EU and UK in turn raises the risk of China and Russia feeling at greater liberty to challenge the West’s belief in its hegemony, and more broadly the Global South to continue to disengage from western influences. It would appear that Israel’s strategy is to fully occupy Gaza and in the process decimate Hamas, but as the Red Sea attacks amply demonstrate, this will only serve to embolden and galvanize militant activity in the Levant and the Middle East, and indeed popular unrest, as well as raising risks for Israel’s long-term security. There is no doubt that these two conflicts will be pivotal to the geopolitical and economic outlook worldwide.

A semblance of normality returned to the global economy, with residual supply chain shock effects largely resolved, or perhaps more realistically ‘largely in abeyance’, given that the structural deficiencies exposed by the pandemic remain, and the fracturing of the global economy, in no small part due to ongoing, and potentially escalating geopolitical tensions. Falling food and energy prices allowed inflation to fall more than expected in the developed, and much of the developing world (excluding Argentina and Turkey), but not back to pre-pandemic levels. The US economy will slow in 2024, but does not seem likely to fall into a recession, while the Eurozone and the UK will continue to flirt with recession. The greater concern remains China, as its very much unresolved property crisis, as well as weak external demand pose an ever greater risk of contagion, with the question being whether it reaches a Draghi type ‘whatever it takes’ moment. India and Brazil remain bright spots, but both face differing infrastructure and capacity constraints.

As was more than obvious in the final two months of 2024, the US Federal Reserve will remain very much ‘primus inter pares’ as far as the developed world rates outlook goes, and by extension financial market risk appetite. The sharp shift in Q4 2023 in terms of rate expectations and bond yields leaves a very large majority of investors positioned for a sharp easing of policy rates, which goes far beyond an adjustment to ensure policy rates are not too high in ‘real’ terms, and implies the need for the Fed and other major central banks to respond to almost certain recession. The latter does not fit with current equity market valuations. That skew in positioning, and a myriad of economic uncertainties look to be a seedbed for volatility, given that central banks remain quite literal in terms of their adherence to 2.0% inflation targets, regardless of the small degree of flexibility that has been introduced in recent years.

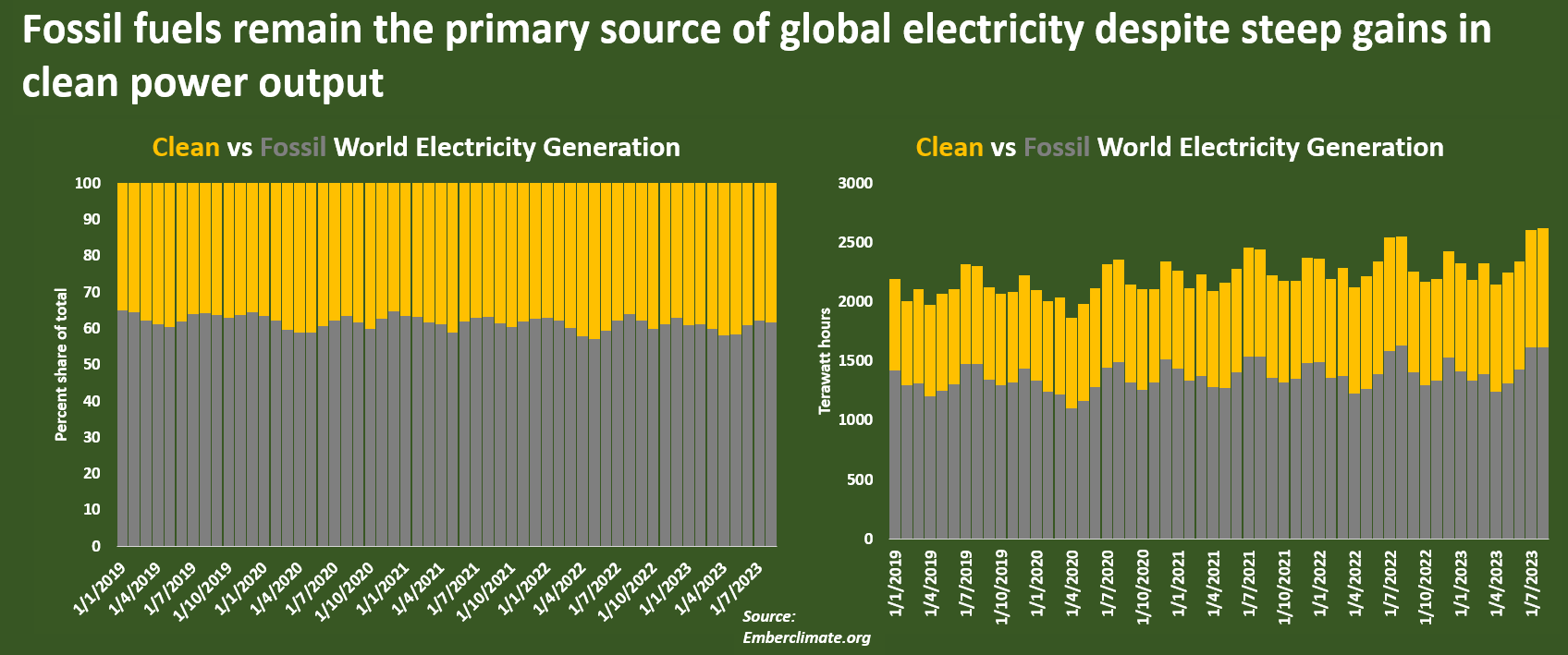

It is already proving to be a very tempestuous, or on the other hand unseasonably warm winter in various parts of Europe, as well as North America and Asia, underlining the potential for further weather related disruptions. While the Red Sea attacks have checked the seemingly relentless downtrend in oil and gas prices, the fact remains that there is such a lot of shuttered OPEC+ crude oil production, and non-OPEC+ production continues to increase, while gas markets look to be in danger of a very large long-term glut, both demand and production related. Nevertheless, the chart that most impressed me during 2023 was that renewable (primarily wind and solar) power production is only just about managing to keep up with increasing power demand. To be sure, planned new renewable capacity should start to tip this balance, but there remains a very large question about whether it will keep up with the likely rapid increase in demand.